How to Tackle Tax Havens

It is hard to crack down on tax havens because powerful actors use them and powerful countries are them. In a globalized world where countries seek to attract mobile capital, they offer financial incentives such as low tax rates, loopholes, and lax regulations. However, the billions of dollars flowing in also harm receiving countries as they spiral into a race to the bottom and create economically extractive financial sectors. Fortunately, there are promising paths for policymakers, corporations, prosecutors, and civil society to take on tax havens, providing a new opportunity for the Joe Biden administration to lead an international coalition.

We are the Tax Havens

On January 1, at the tail end of the Donald Trump presidency, the United States enacted a dramatic anti-corruption measure, the Corporate Transparency Act (CTA). The CTA requires corporations and limited liability companies to disclose their human owners.

Until then, the world’s drug cartels, money launderers, human traffickers, and corrupt officials could incorporate anonymous shell companies in U.S. states for a few hundred dollars, with less hassle than it takes to obtain a library card. These shell companies could evade penalties knowing that no law enforcement agency or tax authority could determine who owned them. The United States has been ranked among the world's biggest tax havens because of the scale of assets held in the country and owned by non-residents in financial secrecy, including via shell companies.

The CTA, although far from perfect, was especially remarkable because most countries crack down on outward leakages and losses to offshore tax havens elsewhere. It is far rarer for the tax haven itself—in this case, tax haven United States of America—to crack down meaningfully on inflows of dirty money.

This context provides clues as to why it has been so hard to crack down on tax havens. The most important tax havens are rich, powerful countries such as Switzerland, Luxembourg, the United States, as well as Britain and its overseas territories such as the Cayman Islands. Powerful countries protect tax havens because they are the tax havens, discreetly hoovering up the world's dirty money for safekeeping. Additionally, in every country, rich and poor, the biggest users of offshore tax havens, and thus the most strenuous opponents of crackdowns, are the wealthiest and most powerful actors.

Yet this is quite an important problem to crack, given the scale of the damage that tax havens inflict. The International Monetary Fund estimated that countries lose up to $600 billion annually in tax revenue from multinationals’ tax haven use. Estimates for the scale of assets held offshore are as high as $42 trillion, effectively beyond national laws’ reach. Allowing elites or criminals to jump offshore to escape domestic rules undermines democracy itself.

The Race to the Bottom

A race to the bottom among tax havens adds to the problem with powerful actors protecting tax havens. Capital is mobile and flows easily across borders, leading states to dangle incentives such as financial secrecy or tax loopholes to attract capital inflows. When one country enacts a stronger or more devious trust law or financial regulatory loophole, relaxes enforcement, or cuts corporate tax rates, others respond with something stronger to remain attractive. This competition leads to the idea that there is a trade-off between democracy and prosperity. If you protect the democratic process and regulate elites, the thinking goes, you fall behind in the race of attracting capital. As the race progresses, the global offshore system becomes increasingly useful to wealthy individuals, multinationals, and criminal groups wanting to escape tax, regulation, criminal laws, or other democratic restraints they dislike. The result is one set of laws for them and another set of laws for everyone else—a recipe for widespread anger.

This race to the bottom is a classic collective action problem, where it is in actors’ collective interests to stop, but where each player has the incentive to cheat to get ahead.

The standard solution to a collective action problem is for actors to collaborate and coordinate. Indeed, the Organisation for Economic Co-operation and Development, the club of rich countries, oversees two main schemes to tackle this race. The first, the Common Reporting Standard, helps countries share information so that each can pierce offshore secrecy and track and tax the assets of its wealthiest taxpayers. The second, the Base Erosion and Profit Shifting (BEPS), seeks to close tax loopholes for multinationals. Both have had some significant successes but also face major weaknesses. Shepherding countries that have strong incentives to cheat is like herding cats. Moreover, it is hard to rally domestic constituencies behind complex international collaborations, especially if the goal is to help other countries.

Another potentially more powerful method to tackle this issue is to start with a strand of the financialization literature known as “Too Much Finance.”

Fresh Thinking: The Finance Curse

Financialization is a well-studied phenomenon where financial tools, techniques, and institutions penetrate deep into non-financial parts of the economy as the financial sector expands. From manufacturing to healthcare to the music industry and beyond, the primary goal is to extract wealth from those sectors instead of productively contributing to them. This extraction, also done via tax havens, is widely known to redistribute the pie upwards to the wealthiest.

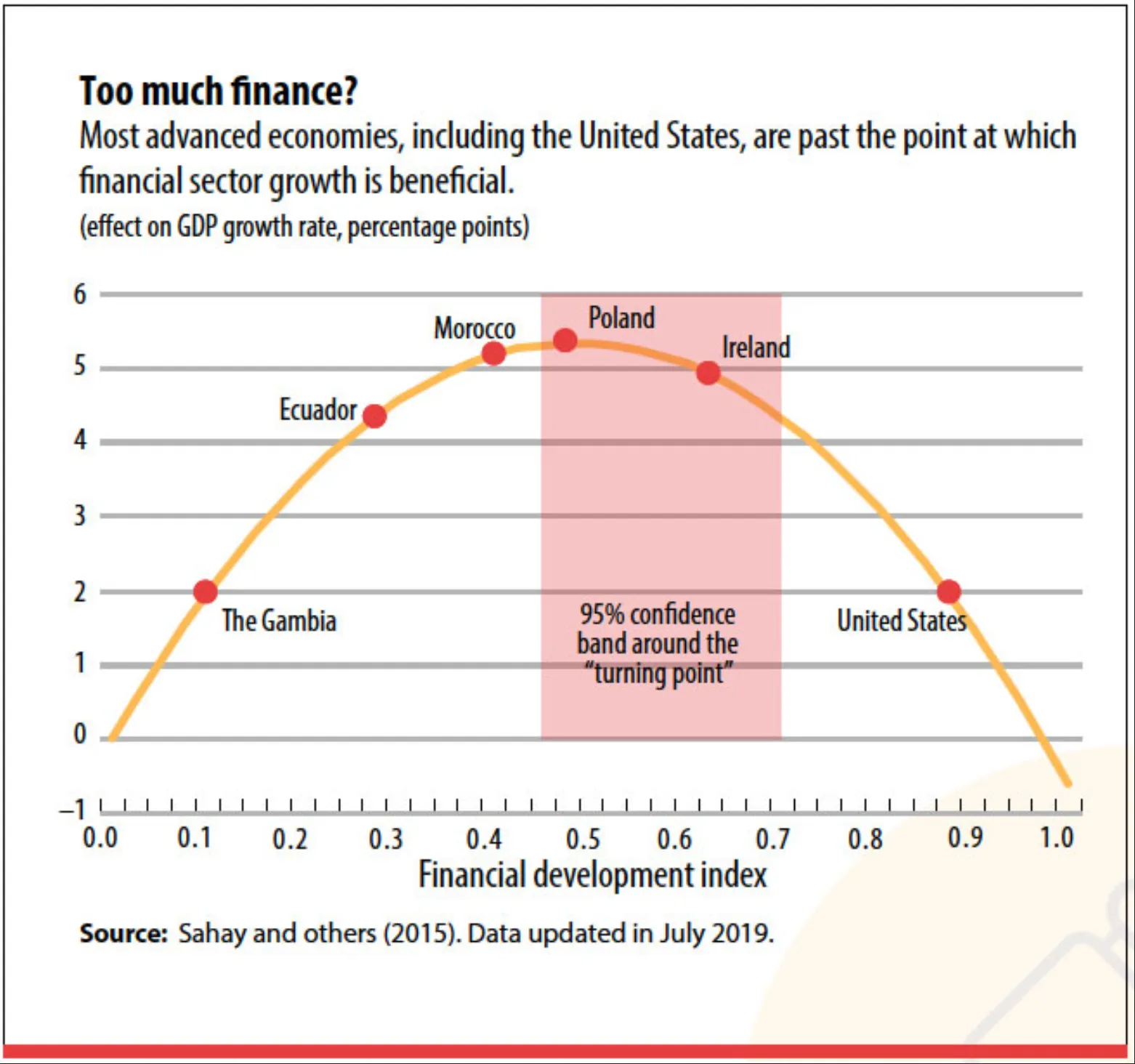

The too much finance literature goes a step further, showing that excessive growth in finance does not only redistribute the pie in harmful ways but that it shrinks the pie overall. In the figure below, the core relationship found in several cross-country studies is an inverted u-shape between financial sector development and economic growth.

Source: IMF

Countries with undersized financial sectors can boost growth by expanding them. But there is an optimal size, which studies suggest is roughly when private credit is equivalent to around 90 to 100 percent of GDP, where the financial sector performs its useful functions. Further expansion reduces growth as extractive and predatory activities grow more dominant and as finance sucks talented people and resources out of other sectors, government, and civil society. The United States and United Kingdom’s financial sectors seem to have passed their optimal size in the 1980s. The effect is an apparent paradox as too much finance makes countries poorer.

Excess finance does not only curb economic growth. It inflicts a broader finance curse, damaging host countries in various other often unmeasurable ways, such as undermining democracy, fostering inequality and crime, or increasing financial instability. An important channel for this harm is through being a tax haven—by degrading taxes, laws, and enforcement to attract foreign capital inflows. There are various harms from such inflows of tainted capital. For instance, they boost inequality by rewarding a small elite of bankers, wealth managers, accountants, and real estate brokers, while pushing up domestic prices, such as those in real estate. These rising prices make goods, such as housing, less affordable for many locals, while a higher price environment makes other tradable economic sectors less competitive against imports. Tainted inflows of capital seeking secrecy threaten national security, including by opening secret channels empowering criminals and other potentially hostile actors to influence and corrupt domestic politics.

The Finance Curse as a Tool to Tackle Tax Havens

The finance curse does, however, provide a novel way to tackle tax havens by opening up anti-tax haven policies that pursue national self-interest. The rich-country tax havens need not debase their taxes and regulations to attract financial inflows. Instead, the finance curse says to do the opposite. The United States must shrink its own financial center down to a useful, economically beneficial size to boost domestic prosperity and protect its democracy. One way to achieve such a smart shrinkage is by curbing tainted financial inflows, or, in other words, by stopping to be a tax haven. This may harm certain domestic interests but will benefit the economy and democracy as a whole.

This analysis slices through the collective action knot and reveals no collective action problem or trade-off between democracy and prosperity. While international collaboration is still a good idea, countries need not wait for others to join collective global schemes. Still, they can act unilaterally, rapidly, and purely for their own good. National self-interest is a far more attractive proposition for voters.

It may be that these kinds of win-win approaches are the only way to tackle tax havens effectively because they have the most reasonable chance of success.

As the issue is not a matter of country versus country, but instead a confrontation between wealthy owners of global capital against ordinary people worldwide, powerful coalitions across the political spectrum can be assembled. From left to right, ordinary citizens can stand shoulder to shoulder to address the issues stemming from both the damaging outflows and the tainted inflows of secret capital. For instance, the coalition that just won the battle against U.S. shell company secrecy is a perfect case of a so-called rainbow alliance; in this case a wide-spreading coalition including national security agencies, left-wing NGOs, police and prosecutors, faith groups, CEOs of small and large businesses, labor unions, banks and credit unions, and many more.

Cross-border mobilization against tax havens is proving powerful too. For example, the OECD's CRS and BEPS projects mentioned above are both the fruits of global campaigning, originally spearheaded in the early 2000s by the Tax Justice Network., This progress has flowered into a global movement involving investors, small businesses, public authorities, anti-crime groups, NGOs, and many others. They collectively exerted enough pressure to drive changes at a global level. In recognition of its efforts and successes, this past January, the international tax justice movement was nominated for the Nobel Peace Prize.

Policy Implications for the Biden Administration

The Joe Biden administration can draw several lessons from the efforts and successes to pursue effective policies. In the broadest terms, the finance curse could unlock the reforms that large majorities of voters demand, such as greater transparency, stronger protective financial regulations, higher taxes on financial capital and its owners, and better enforcement of all of the above. It is also a useful filter for sorting out responsible investors—who accept such policies as the reasonable price of doing business—from bad actors—who run away from them. The finance curse shows us that such reforms do not just protect democracy and curb inequality but also boost economic growth.

The United States should effectively join the previously mentioned Common Reporting Standard. Currently, the United States has a technically similar system called the Foreign Account Tax Compliance Act, which powerfully leverages information about the U.S. taxpayers’ financial assets abroad. However, the United States sends relatively little information to other countries in return. By unblocking this pipeline of information, the United States would be less welcoming to hostile actors and their tainted money, protect itself from this dangerous finance, and earn international goodwill. Similarly, it could relax its long-running efforts to prevent foreign countries from taxing Facebook, Google, and other dominant U.S. firms, and instead, crack down on the tax havens they use.

Another example of a worthwhile policy effort would be to dust off the anti-money laundering Rule 1506-AB10 that the U.S. Financial Crimes Enforcement Network proposed in 2015, but laid dormant under the Trump presidency. This rule would require hedge funds and private equity firms to establish strong anti-money laundering programs, report suspicious activities, file currency transaction reports, and keep proper records. Currently, such firms are exempt from money laundering rules on banks, allowing them to attract tainted and secretive capital from overseas, including from Mexican drug lords and Russian mobsters, while hardly raising eyebrows. They then typically channel these funds through extractive strategies that harm U.S. workers, consumers, and even investors.

Such measures to curtail tainted financial inflows could usefully pit the Biden administration, alongside the rainbow coalitions in the United States and abroad, against wealthy and predatory financial interests, rooted in Wall Street, the City of London, and offshore. These kinds of implicit finance curse approaches would be both beneficial and politically popular for Biden, at home and abroad. Popularity abroad matters as the United States needs to lead its European counterparts. Britain is pushing to relax financial regulations after Brexit. In the European Union, several member states, including Luxembourg, the Netherlands, and Ireland, are leading tax havens, which routinely block meaningful financial regulations in the EU.

A Better Path Forward

Around the world, financial government policies lie on a spectrum between two poles. One is the upgrading path, which focuses on improving public goods such as education or infrastructure to improve economic performance. The other downgrading path is that of the tax havens, offering tax loopholes, lax regulations, or downgraded enforcement to lure mobile capital. The former approach focuses on one's citizens; the latter race-to-the-bottom variant prioritizes plutocrats. The CTA has nudged the United States in the upgrading direction, but there is still space for the Biden administration to show leadership here, both by cracking down on foreign tax havens across the world and by picking fights at home with Wall Street, in a broad effort to tackle the finance curse currently convulsing its politics. A wonderful by-product would be to set up the United States, currently one of the largest tax havens, as the recognized leader in the global fight against tax havens.

Nicholas Shaxson is a journalist specializing in politics and financial globalization. He is the author of Treasure Islands and The Finance Curse. He has written numerous articles for the Financial Times, Vanity Fair, Economist, Washington Post, Guardian, the IMF, and many others. He works part-time for the Tax Justice Network, an organization that campaigns against offshore tax havens.