Brazil, Mexico, and COVID-19: A Striking Contrast

Brazil and Mexico experienced the first signs of the COVID-19 pandemic roughly at the same time. A year later, Brazil is one of the countries that has provided the most financial support to its population during the pandemic and Mexico is among the countries that have spent the least. Yet, the increase in debt as a proportion of GDP in Mexico is similar to Brazil’s, highlighting the great paradox that austerity will not bear the expected fruits and actually increase the national debt in the same manner greater spending would. The different approaches resulted in Brazil’s economic downturn being smaller, the recovery faster, and the increase in inequality and poverty lower. Despite Brazil’s worrisome surge of COVID-19 infections in early 2021, the fact remains that fiscal policy curbed the fall in living standards to a greater degree in Brazil than in Mexico.

Response to the Health Crisis: Similarly Dysfunctional

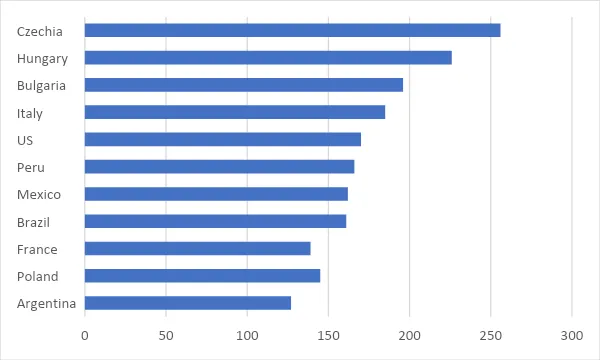

One measure of the overall effectiveness of the policies undertaken by Brazil and Mexico is the number of COVID-19 deaths per 100,000 inhabitants, which is tracked by John Hopkins University. As shown in Figure 1, Brazil and Mexico both fared poorly in saving lives. However, studies of excess deaths by The Economist and others suggest that Mexico could have suffered as much as twice the number of officially reported deaths. In contrast, Brazil may have underreported only by 10 to 20 percent. This implies that Brazil has outperformed Mexico on this metric.

Figure 1. Reported deaths from COVID-19, per 100,000 inhabitants, cumulative data as of April 7, 2021.

Source: John Hopkins University Coronavirus Resource Center.

Economic Responses: On Opposite Ends

Fiscal, monetary, and credit policies

Government measures to mitigate the pandemic’s economic impacts have been far greater in Brazil than in Mexico. In March 2020, the Brazilian Congress declared the pandemic a “public calamity.” This allowed the government to exempt the budget from reaching its deficit goal in 2020 and the Fiscal Responsibility Law requirements. In total, Brazil’s fiscal and liquidity support measures add up to 14.6 percent of 2020 GDP, making it one of the largest counter-cyclical packages in the world.

By contrast, the Mexican government allocated much fewer resources to support its economy during the crisis. The government provided loans to family businesses, unemployment insurance to workers with debt to the National Housing Institute, and delivered infrastructure investments. In total, Mexico’s fiscal and liquidity support measures add up to 1.1 percent of 2020 GDP, making Mexico one of the countries providing the least economic support to its population during the pandemic.

Impact on economic growth, public debt, and inflation

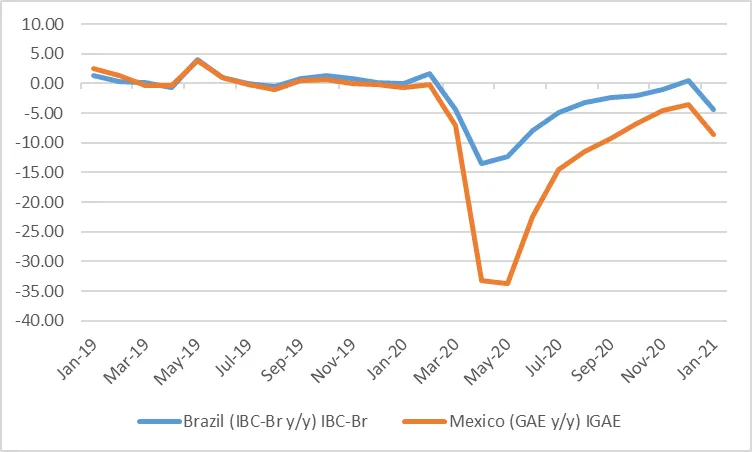

While the pandemic resulted in a drastic decline in economic activity in both countries, Figure 2 shows that the decline in Brazil has been shallower, and the recovery faster than in Mexico. These contrasting growth trends are highlighted by the International Monetary Fund’s forecasts for 2021 through 2025, which estimate that Brazil’s GDP declined by 4.6 percent during 2020 and will recover by 3.7 percent in 2021. In comparison, Mexico saw an 8.5 percent drop in 2020 and is projected to rebound by 5.0 percent in 2021. If we combine 2020 and 2021, Brazil will have a compound fall of 1.1 percent while Mexico’s would be 3.9 percent, as seen in Figure 3.

Figure 2. Recent indicators of economic activity in Mexico and Brazil, 2019-2020

Source: INEGI.

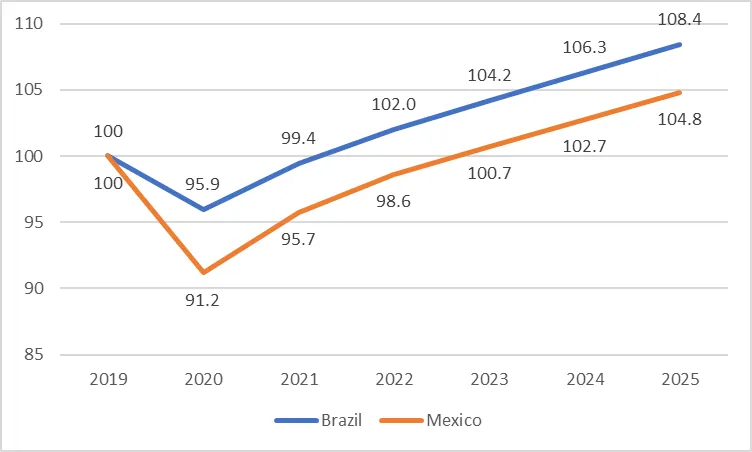

From 2022 to 2025, the IMF expects both countries to grow at similar rates, slightly above 2 percent. However, as shown in Figure 3, where GDP was indexed in the two countries to 100 in 2019, Mexico would recover to 2019 GDP levels in 2023, roughly two years later than Brazil, and more than three years after the start of the pandemic.

Figure 3. Forecasts of GDP levels for Brazil and Mexico, 2019 = 100

Source: Calculations with IMF data, World Economic Outlook, April 2021.

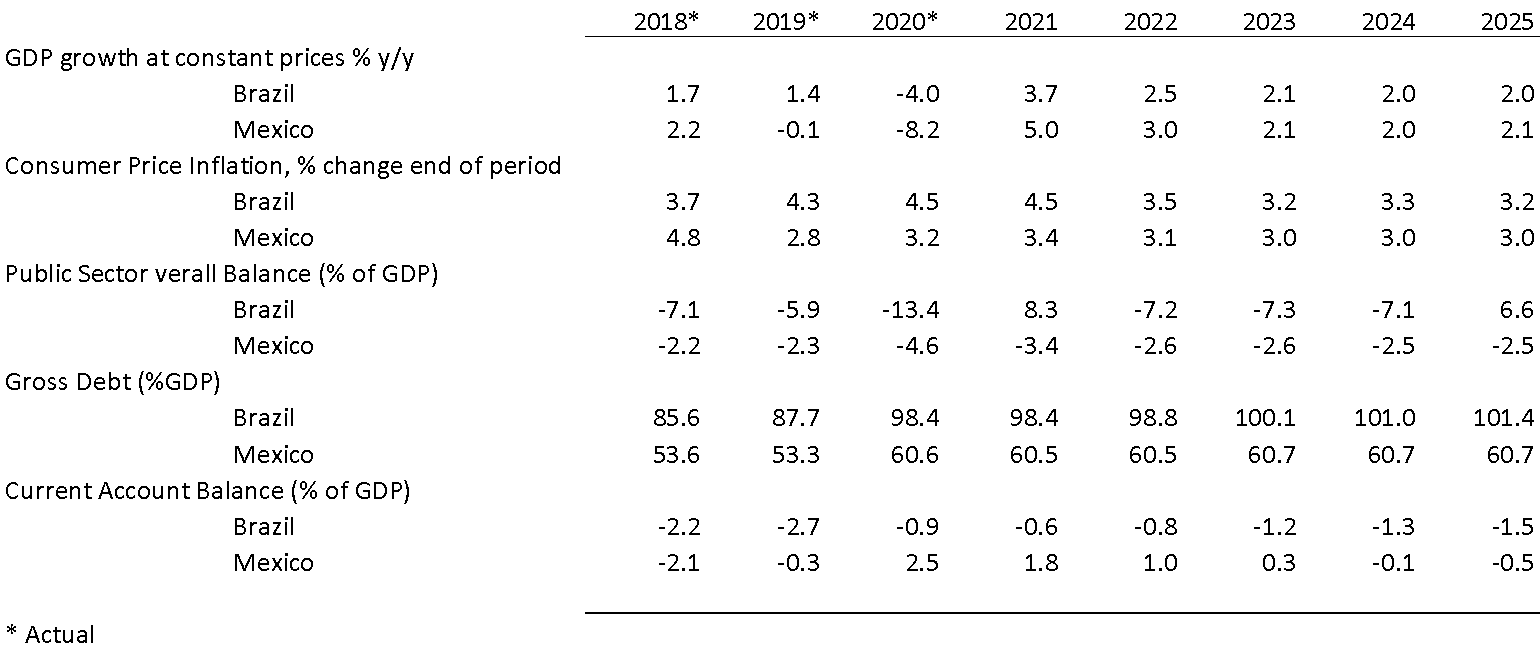

Moreover, an overview of the main macroeconomic variables for both countries can be seen in Table 1. Interestingly, Mexico experienced an increase in inflation in 2020 despite its large output gap, while Brazil saw a decline. Brazil’s inflation is expected to remain stable, around 4.5 percent in 2020-2021. From 2022 to 2025, the IMF inflation forecasts in both countries are similar. Despite the Mexican government’s austerity efforts, its budget deficit increased by 2.3 percentage points of GDP, from 2.3 percent in 2019 to 4.6 percent in 2020. As Mexico’s fiscal support package was only 1.1 percent of GDP, the deterioration in this ratio is explained by the fall in 2020 GDP. Brazil’s debt to GDP increased from an already-high level of 88 percent in 2019 to 98.4 percent in 2020, or 10.4 percentage points. For Mexico, the IMF estimates that the debt rose from 53 percent to 60.6 percent of GDP, an increase of 7.6 percentage points of GDP.

Table 1. Summary of macroeconomic variables and forecasts for Brazil and Mexico 2018-2025

Source: IMF World Economic Outlook Database, April 2021.

Financial markets reaction

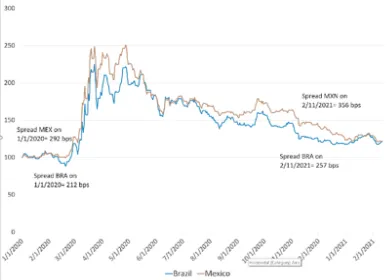

Financial market indicators provide another picture of how the different approaches by Mexico and Brazil have panned out. As seen in Figure 4, sovereign bond spreads over U.S. Treasuries for both countries have moved largely in tandem during the span of the pandemic, suggesting that credit markets have not significantly punished Brazil for its large pandemic relief package, nor have they rewarded Mexico for its austerity.

Figure 4. Sovereign spreads in Brazil and Mexico during the Pandemic

Source: Calculations with JP Morgan, Bloomberg data.

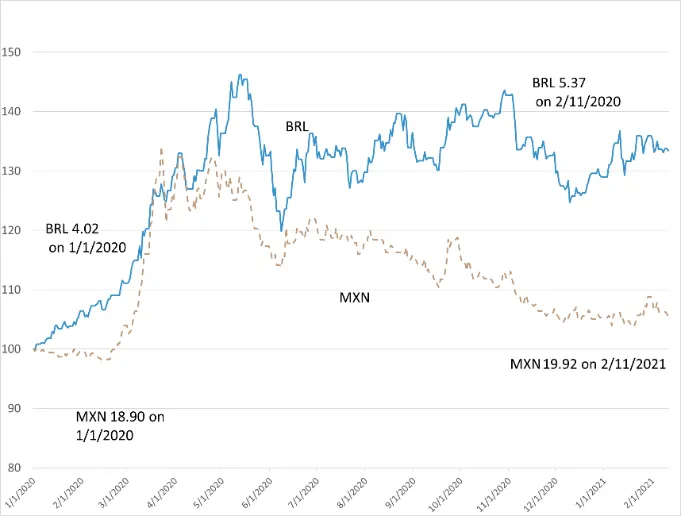

Compared to the other economic and financial indicators, currency and stock markets have actually favored Mexico over Brazil. For instance, Figure 5 shows how, between January 2020 and February 2021, the real depreciated 33.4 percent against the dollar compared with only a 5.4 percent depreciation for the peso. This may be due to the differential interest rates in Mexico versus the United States and the surprising performance of remittances from Mexicans in the United States, up 11 percent in 2020. In Brazil, the aggressive interest rate cuts by Banco Central do Brasil and the fall in the price of raw material exports negatively impacted the real.

Figure 5. Currencies in Brazil and Mexico during the Pandemic

Source: Calculations with JP Morgan, Bloomberg data

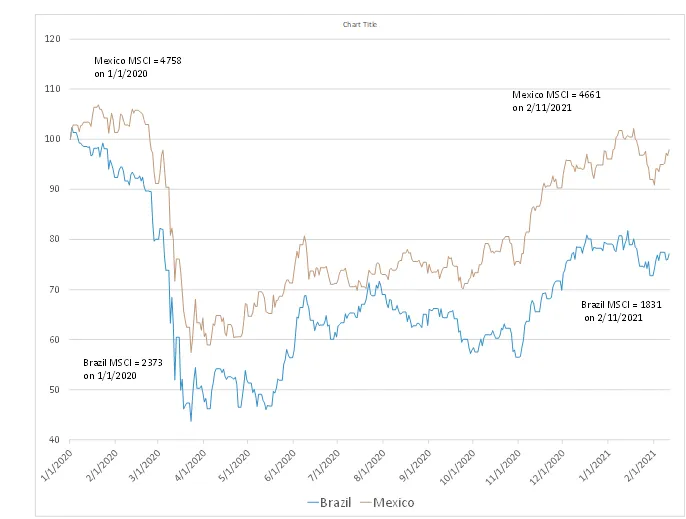

Similarly, Figure 6 shows how Mexican stocks outperformed Brazil’s by about 23 percent in dollar terms. This is largely due to the underperformance of the real against the peso and the more counter-cyclical main components of the Mexican index, which are telecoms, media, and consumer staples, compared to Brazil’s more cyclical components, such as commodities and financials.

Figure 6. Stock markets in Brazil and Mexico during the Pandemic

Source: Calculations with JP Morgan, Bloomberg data

The contrasting approaches to government support during the pandemic between Mexico and Brazil have resulted in different paths during the downturn, with a favorable economic recovery for Brazil. Credit markets show that Brazil’s fiscal efforts were not penalized, nor was Mexico’s austerity rewarded. Although the currency and stock markets did favor Mexico, this seemed to be caused more by high-interest rates, well-performing remittances, and the type of counter-cyclical products and services of public companies, rather than international trust in or domestic success from Mexican austerity policies

The Social Cost of COVID-19: Mexico Sees More Damage

Policies to protect formal and informal workers

The Brazilian government enacted substantive and unprecedented measures to protect the livelihoods of both formal and informal workers. The government instituted a subsidy program to maintain formal employment, consisting of minimum wage payments to temporarily suspended workers or whose working hours were reduced. By August 2020, 16 million workers were covered by this program.

The government's efforts to support informal workers went even further. Bolsa Familia, a conditional cash transfer program, expanded to include 1.2 million people who had been on the program's waiting list. The government also launched a new temporary cash transfer program, Emergency Aid, or Auxílio Emergencial, in April 2020, which targeted low-income informal workers, self-employed workers, and those already registered with Bolsa Familia, who were eligible to receive a higher amount through Emergency Aid. In 2020, spending on the program was around 4 percent of GDP, reaching almost a third of Brazilians. Emergency Aid is by far the largest social protection program to mitigate the effects of COVID-19 in Latin America. The monthly transfer of 600 reais, which equals about $107, represents about 120 percent of the national poverty line.

The Mexican government’s social protection response to the pandemic differed radically. In the case of formal workers, the Mexican government’s strategy was to emphasize the application of the rights of workers already enshrined in the Labor Code. The government prohibited layoffs, suspensions, or reductions in hours worked in response to the crisis. The government only granted loans of 25,000 pesos, around $1,134, to one million people with small and medium-sized enterprises in formal and informal sectors, spending around 0.9 percent of its GDP.

There were practically no measures to mitigate the impact on the informal sector. The amounts of transfers in existing programs were not increased, nor were new programs offered to cover workers or households in the informal sector. The only additional benefit came in the form of allowing an advance of pension payments for the elderly and the disabled at several points during 2020 and a slight expansion of a cash transfer program for farmers. Faced with the inaction of the federal government, state governments have introduced their own social protection programs. Many Mexican states provided cash transfers and food assistance to their populations and created temporary employment programs, but the reach and coverage of these programs were too small to have a meaningful impact.

Impacts on inequality, poverty, and educational attainment

In their paper for the Center for Economic Policy Research, Lustig, Martinez Pabon, Sanz, and Younger conducted micro-simulations that suggest that Emergency Aid potentially mitigated the pandemic’s negative effects on inequality and poverty in Brazil in 2020. In the absence of any mitigation measures, inequality would have increased from a pre-pandemic Gini coefficient of 0.55 to 0.56. As measured by the international poverty line of $5.5 per day in purchasing parity dollars, poverty would have increased from around 25 percent to around 28 percent, and the number of poor could have increased from 53 million to 57.6 million. Notably, the micro-simulations show that given the size of Emergency Aid, both inequality and poverty could turn out to be even lower than pre-pandemic levels once the expansion of social assistance is considered. Inequality could have decreased their Gini coefficient from 0.55 to 0.54, and 4.3 million people could be lifted out of poverty. Contrastingly, in Mexico, the same micro-simulations estimated that the incidence of poverty could have potentially increased from around 35 percent to 42 percent for 2020, the number of poor could have increased from 43.6 million to 52 million, and inequality could have risen from a pre-pandemic Gini coefficient of 0.46 to as much as 0.48.

Beyond the short-term impacts on inequality and poverty, the pandemic could have lasting effects on poor Brazilian and Mexican children due to the impact on human capital. According to previous research at the CEQ Institute, the pandemic could reduce the probability of completing secondary education from 57 to 23 percent in Brazil and 54 to 24 percent in Mexico for children from households with low-educated parents. In contrast, for children from households with parents who have completed high school or more, the probability of graduating from secondary education is nearly 90 percent and remains almost unchanged by COVID-19. That is, the inequality of opportunity looks almost equally grim for both countries.

Conclusion

Even though Brazil and Mexico have followed similar, although flawed, health policy approaches to COVID-19, they have pursued vastly different strategies to mitigate the economic and social consequences. At the one extreme is Brazil, which implemented counter-cyclical fiscal policies of considerable magnitude, well above the global average. An important component of this policy has been the increase in spending on social assistance to both formal and informal population segments, perhaps too much since the assistance reached non-poor individuals who may not have needed it. Mexico is at the opposite pole; the fiscal package has been exceedingly small and social assistance has not been meaningfully increased. All of this mitigated the negative impacts on growth, employment, and poverty in Brazil, although not in Mexico. Importantly, Brazil's expansionary policy, although it may pose a challenge to debt sustainability, has not resulted in significantly higher inflation and is not expected to do so in the future. In Mexico, the goal of keeping its debt-to-GDP ratio constant was not achieved due to the sharp drop in economic activity.

As of April 2021, the trend of new COVID-19 infections is down in Mexico, while Brazil is experiencing an alarming surge in infections which could affect its pace of economic recovery in the future. For both countries, the immediate priority is to quickly conclude national vaccination campaigns to control the pandemic. Both countries need to overcome limited vaccine supplies to accelerate their vaccination campaigns.

Once the pandemic is under control, Brazil’s most important challenge will be to navigate the return to a sustainable debt trajectory without offsetting factors supporting economic growth and human development. Mexico’s most important challenge will be to ignite the lacking public and private investment to achieve higher growth. This will be needed to recover the years of economic and social progress lost during the pandemic. Policymakers can learn that in the face of a severe economic crisis, the pursuit of fiscal austerity for its own sake can be counterproductive and result in lower growth and, paradoxically, higher indebtedness.

Nora Lustig is Samuel Z. Stone Professor of Latin American Economics and Founding Director of the Tulane University Commitment to Equity Institute. She is also a senior non-resident fellow at the Brookings Institution, the Center for Global Development, and the Inter-American Dialogue. ([email protected]; @noralustig)

Jorge O. Mariscal is an Adjunct Professor at the School of International Affairs, Columbia University. He is the former Chief Investment Officer for Emerging Markets at UBS Global Wealth Management. Dr. Mariscal obtained a Ph.D. in economics from New York University. ([email protected]; @jorgeOmariscal)